Question for Your Advisor (and yourself): Is my Plan Protecting My Family and My Assets?

Most people don’t have an estate plan. I get it. It’s tedious, no real-time benefit, it costs money. While important, it’s not urgent.

I get it.

Estate planning is one of the few areas of your financial life where choosing inaction doesn’t feel like a decision - but choosing not to act actually is a decision.

It’s a decision to let the probate court decide for you - in full view of the public. It’s a decision to let state law default to their convenience, rather than your wishes.

Here’s a simple test. Can you answer these questions right now, without looking anything up?

IF YOU’RE STARTING FROM SCRATCH

Who inherits your assets if you die tomorrow? Not who you ‘want’ to inherit them — who actually inherits them under your current documents and account titles?

If you became incapacitated today, who has the legal authority to pay your bills, manage your investments, and make medical decisions on your behalf? Is that authority documented, signed, and findable?

Do your beneficiary designations on your IRA, 401(k), and life insurance match your intentions — or do they reflect a relationship from ten years ago that no longer exists?

What happens to your minor children if both parents are gone? Is the guardian named in a signed document, or is it just a conversation you’ve had?

When your heirs receive their inheritance, do they understand whether it comes to them pre-tax, post-tax, or somewhere in between — and what that means for the number they actually keep?

If there’s doubt, there is no doubt - you need an Estate Plan.

IF YOU ALREADY HAVE A PLAN

When did you last review it? If the answer is “when I signed it,” that’s the problem.

You may need a refresh on your Estate Documents if….

….you or your children have gotten older.

…your applicable Federal and State laws have changed.

…your portfolio value is bigger.

…you are no longer in good graces or trust people you have listed in authority.

…you started or sold a business.

…you or parties of interest have moved to a different state.

The gap isn’t a lack of intention or discipline. It’s a lack of attention, urgency, time, and structure.

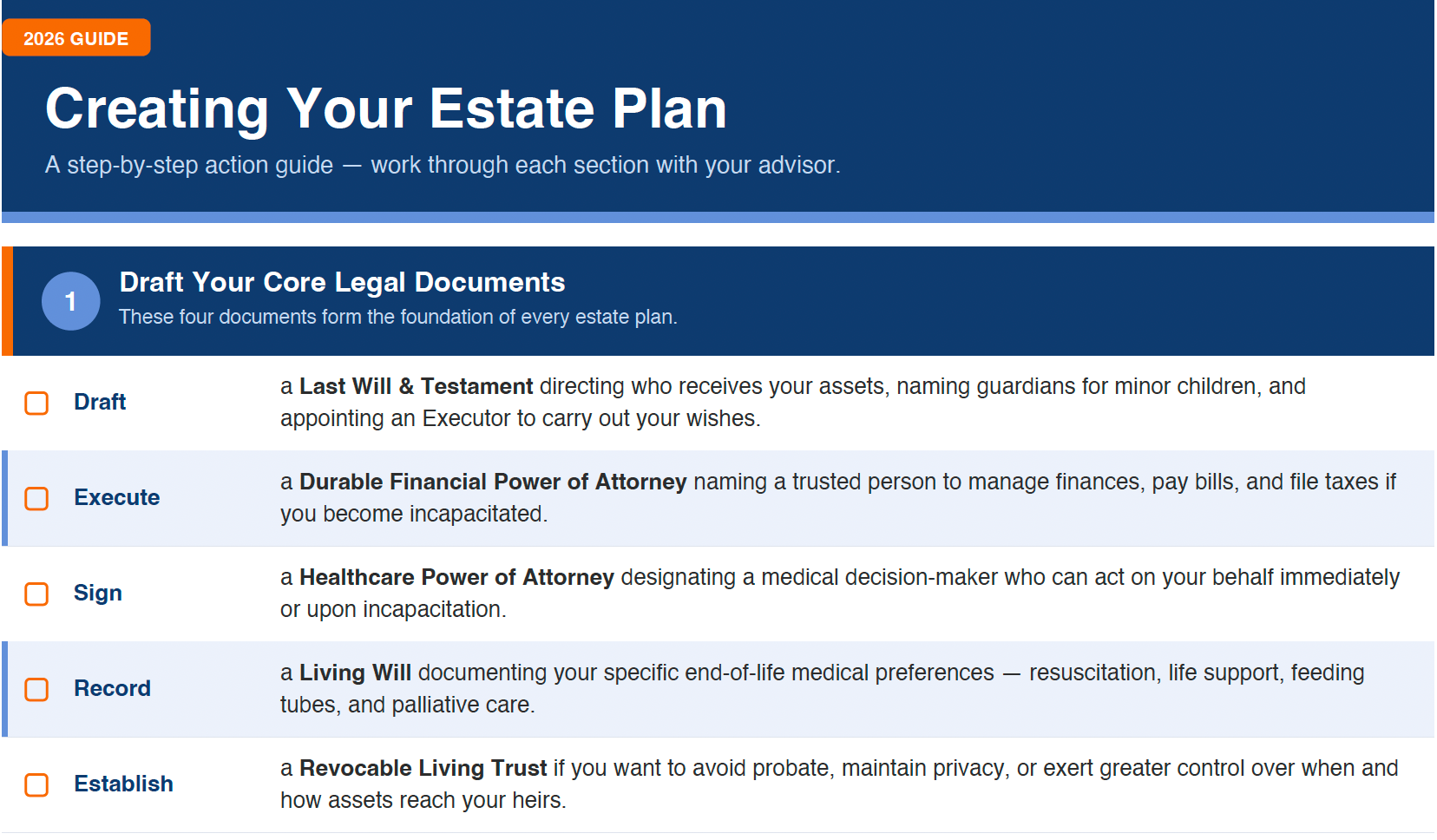

Creating an estate plan isn’t complicated — but it does require working through things in the right order. At its core, it’s four essential steps.

Draft Your Core Legal Documents

Appoint Key People

Align and Establish Triggers for All Asset Transfers

Address Your Unique Circumstances

Create a Clear Tax Strategy that considers your beneficiaries

Reviewing an existing plan is equally systematic: reassessing your people, revisiting your documents, realigning your assets, and responding to the life events that demand an immediate update — marriage, divorce, a birth, a move, a new diagnosis.

In both cases, the structure matters. A checklist you’ve worked through with an advisor is worth far more than a document sitting in a drawer that no one has read in six years.

Two documents. One conversation.

I’ve put together two resources — one for people building a plan from scratch, and one for people who have a plan but know it’s time for a real review. Both are action-oriented. Both are specific. Neither talks around the hard parts. They are meant to catalyze conversations or outline the consequences of avoiding them.

If you’d like a copy of either — or both — just reach out. Reply here or send me an email, or drop me a note at jc@myfinancialstrategies.com. No form to fill out. No sales pitch attached. Just a practical resource that might be the push you — or someone you care about — has been waiting for.

Here’s a tease of Section 1 of the Creation Document.

Estate plans aren’t urgent until they are. Estate plans do what many are looking for in their investments - they reduce uncertainty.