Question for your advisor: How do you evaluate your choices in my portfolio?

Performance and Paradigms are convenient defaults over Process and Priorities

The following is for educational and entertainment awareness, not investment advice. I likely don’t have a damn clue what your situation is and this may not work in your case, so see what you can learn and ask your advisor or yourself what is best for you.

I really don’t give a frog’s fat ass if I beat the S&P500.

I consider diversification a tool that should allow people to stay invested for the long-term- both rationally and emotionally. What matters is the methodology of how that tool is used to allow that. Much like a dental hygienist switches between various instruments…and isn’t afraid to go back and forth given the situation….to get the best possible result for your fangs, which are different from everyone else’s.

So what do I do? I have five unique “firewalls” against stock and bonds (as well as the other firewalls) where I have a portion of the portfolio carved out to challenge the ability of that investment to improve results (notice I didn’t say performance) over stocks and bonds.

I then measure (1) how often was this trade correct, (2) how many days were spent in the right trade, and (3) how much of a lift did it provide.

When I do this collectively, we should find a portfolio that clients feel is getting the job done, even when the S&P500 hype sizzle is getting more attention than our steak.

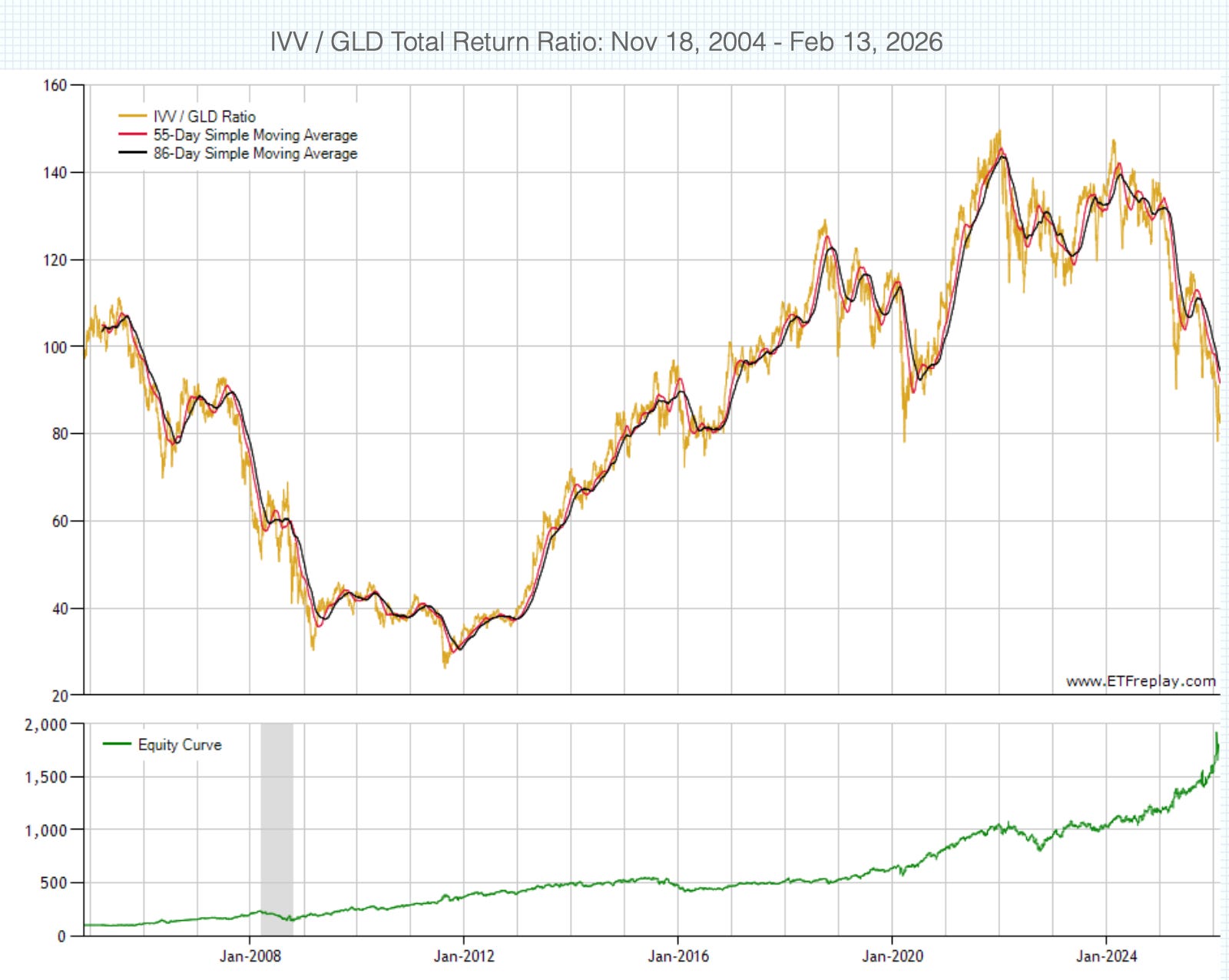

Let’s go through one example: Gold vs. S&P500

The way my models work is that you switch between Investment A (S&P500) and Investment B (Gold), any time the red line crosses the black line. This has happened 70 times in 20 years…that is a lot of trading. Some of these, based on abrupt moves, lasted less than 20 days, and was obvious and probably an intuitive over-ride, but we’ll keep things pure in this example.

As you can see, some of this is a roller coaster leading to false reads based on the model’s sensitivity readings.

How often was the model “right” to switch?

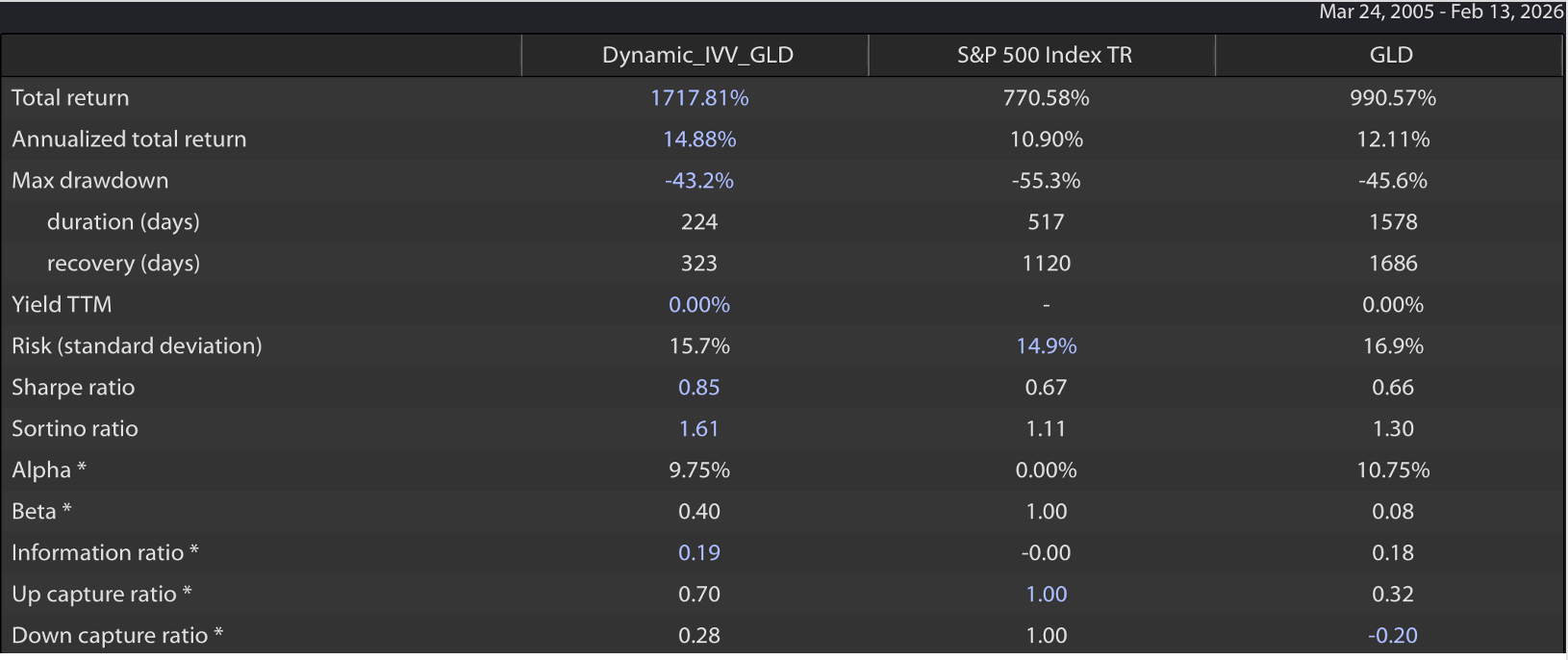

The model was only correct 47.14% of the time.

What % of days was the model in the right trade?

66.61% - given this higher percentage indicates that the model pivots correctly.

Lastly, what is the lift that this approach provides over buy and hold in the S&P500?

Couple of observations:

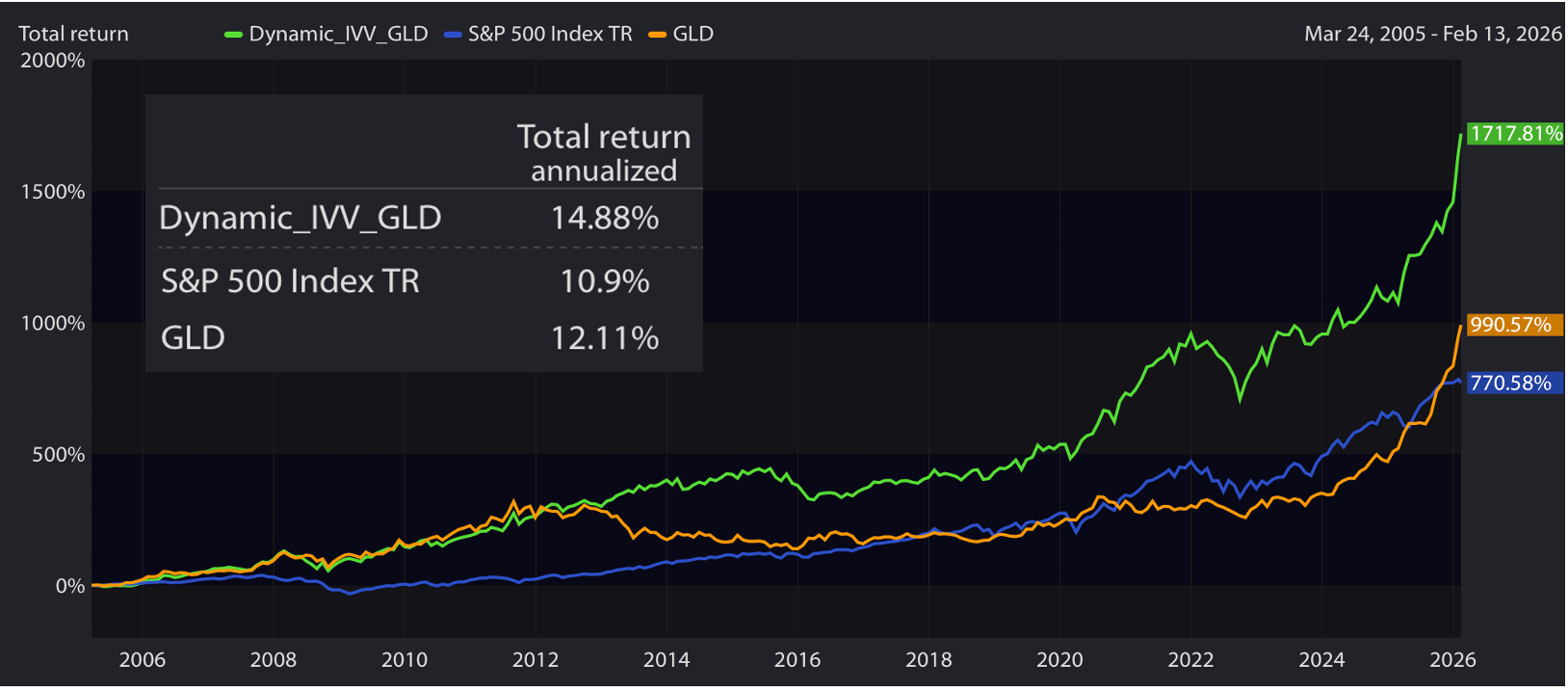

Probably few people would know that Gold has beat the S&P500 in a buy and hold scenario over the past 21 years.

This model had the wrong pick more than 50% of the time, but more than doubled the return of the S&P500.

Imagine having a strategy that captures 70% of the upside, but only 28% of the downside vs. the S&P500.

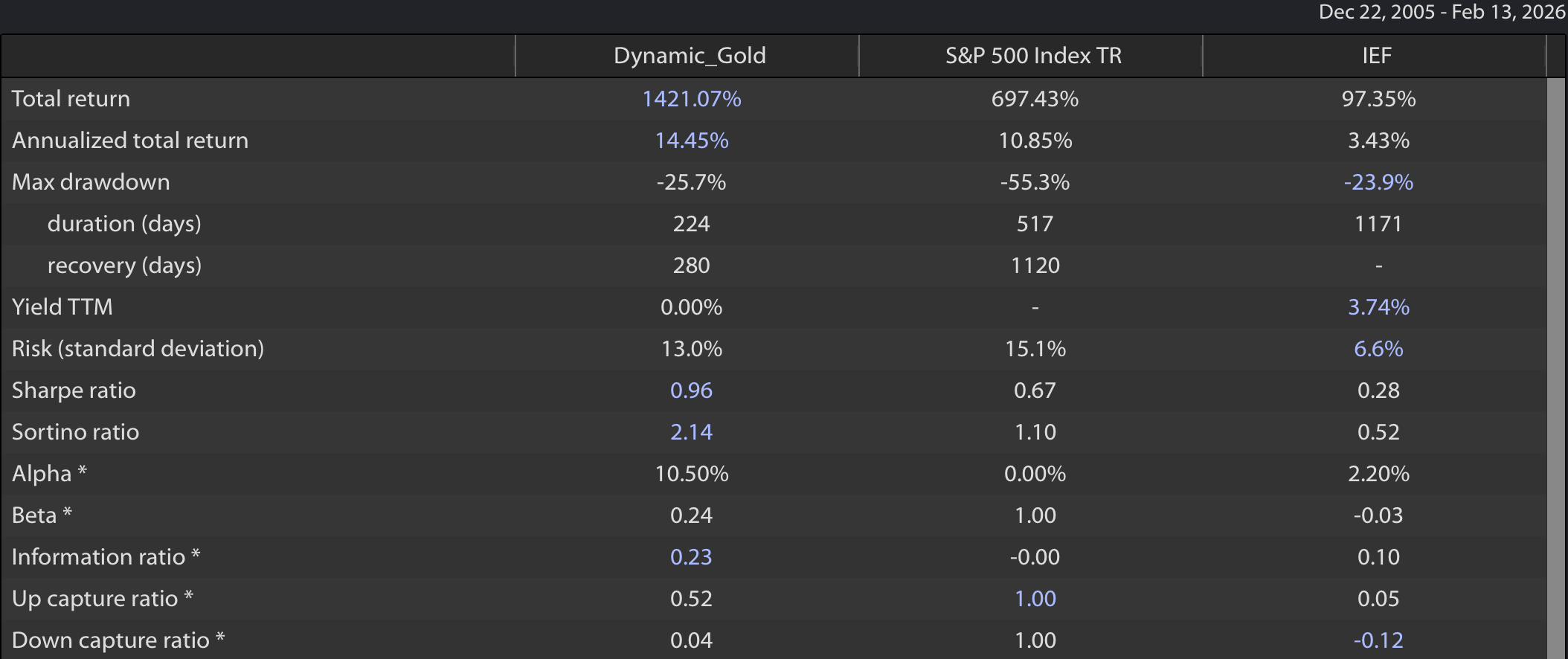

I said earlier that I run this challenge with firewalls like Gold against stocks and bonds. How do these results change when I have the Stock/Bonds/Gold Challenge working in tandem?

The return goes down slightly, but the Max Drawdown goes down significantly.

The Bond-Gold Model, IEF v. GLD, only has the right pick 46.66% of the time, but is in the right pick 80.66% of the time.

The combined impact of these models over the past 20+ years captures 52% of the upside, but only 4% of the downside of the S&P 500.

I have created this process for the S&P500 and IEF (7 to 10 year US Treasury Bonds) against Gold, Managed Futures, International Stocks, and Commodities.

In closing, Roger Federer over his career only won 54% of his points, but won 82% of his matches. Investing can be the same way.