Values, Goals, and Risk Tolerance are crap. Priorities, Trust, and Mindset define your spending and investing of money

“Money is the most universal and most efficient system of mutual trust ever devised.” - Harari, Sapiens - Quoted, Footnoted in Dr. Daniel Crosby’s Book, The Behavioral Investor

Our dominance as a species is built on a shared trust in fictions. One fiction reigns supreme…money. This is another concept introduced by Dr. Crosby.

Money and Trust. It’s difficult to give or receive one without the other. Giving money shows up in many forms and we see that in how we spend.

Dr. Crosby’s Standard Deviations Podcast (author of The Soul of Wealth and The Behavioral Investor) featured Joe Duran, Founder of Rise Growth Partners, put spending money into three categories.

To avoid pain

To enjoy life

To take care of our responsibilities

I spent a lot of time challenging these buckets, thinking that they weren’t mutually exclusive or completely exhaustive. I could argue they are not, but that is subjective style coming into play. It’s really an emotional play with these characteristics. One is to avoid negative emotions, one is to gain positive emotions, and one is transactional. Outside of taxes, Ticketmaster, and credit card convenience fees, it’s hard to say that all of these don’t involve some significant degree of trust. When it comes to trust, often your voice is your wallet and watch.

We must break three paradigms to have a better relationship with our spending and investing.

Paradigm Buster #1: Priorities over Values and Goals

Unfortunately, the Financial Planning Industry dodges the element of trust by using terms like “Values” and “Goals”. Value and Goals aren’t a currency….trust is. Trust is spent on your priorities.

Paving the driveway isn’t a value or goal, but it is a priority that requires money that is aligned with taking care of responsibilities. Who you select to pave your driveway likely has an ingredient of trust in the blacktop.

Paradigm Buster #2: $’s over %

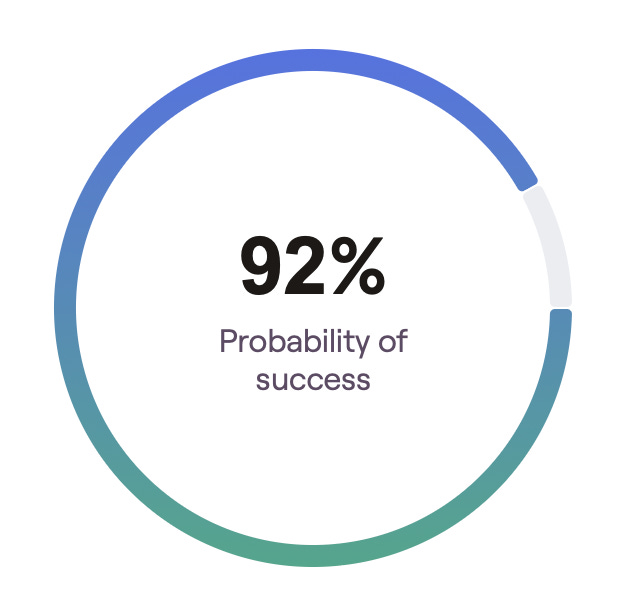

I am going to let this speak for itself. If you have a financial advisor, ask yourself two questions: (1) Which one is you advisor more likely to show you, and (2) Which one is more meaningful? (3) Which one is easier to trust?

Option 1, Probability of Success in Retirement:

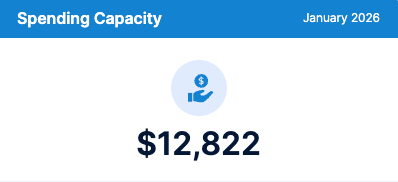

Option 2, Monthly Spending Capacity in Retirement:

Option 2 is an output of Income Lab and I am having much better conversations with clients because $ speaks to trust and priorities. % speaks to probabilities and ambiguities.

Paradigm Buster #3: Risk Tolerance vs. Money Mindset

Here is the biggest thing I have discovered with Risk Tolerance - it seems that it changes most based on if “your guy” is or isn’t in the White House.

Money Mindset seems to be more durable.

Do yourself a favor and take this short quiz to see what your results are (link).

With these results, we can now have meaningful conversations of how we devote not just your present day cash flow, but also your future day cash flow with your investments and your priorities.

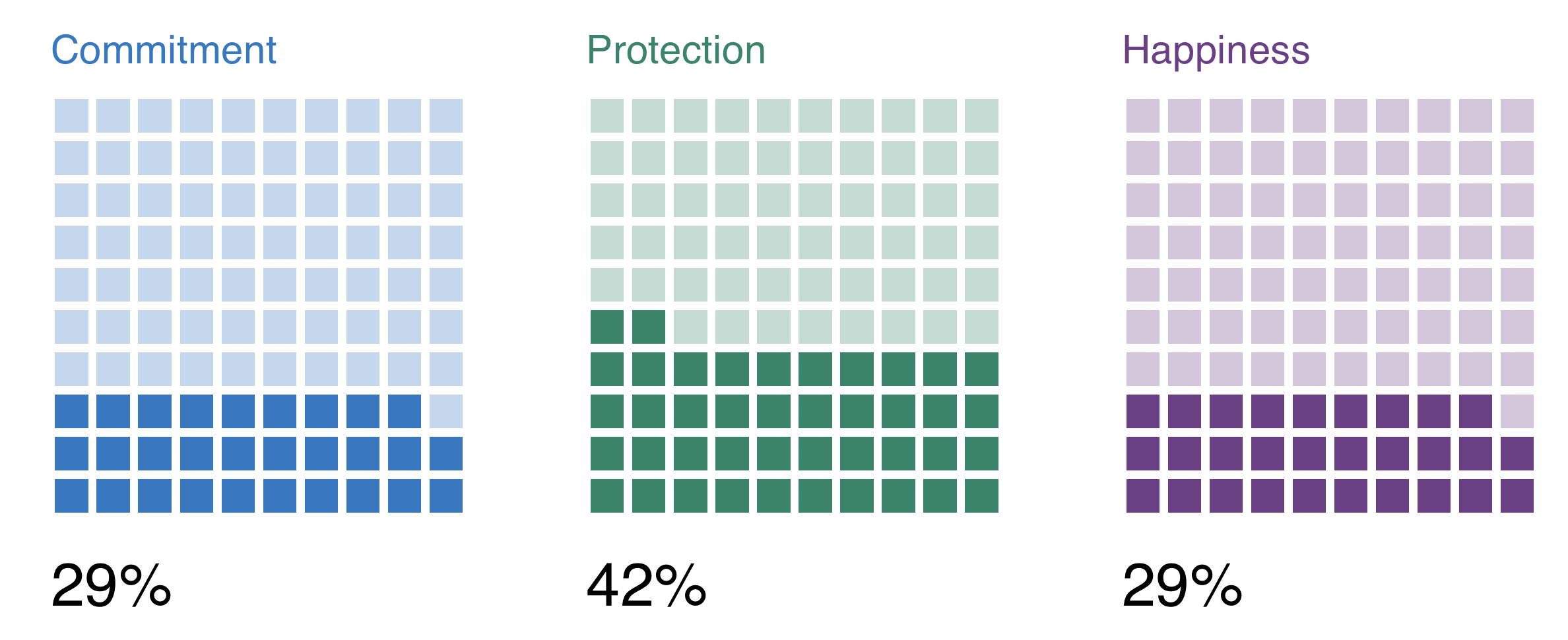

Risk Tolerance as a number and a percentage offers no context. Risk Capacity (how much of a loss you can absorb) is actually more useful.

This graphic allows me to dig into topics like Portfolio Allocation and if that would serve the purpose of Protection, Happiness, and Commitment.

Paradigm Buster #4: Fulfillment over Happiness

Jerry Seinfeld’s son once asked him mom, “Does dad enjoy anything?”

We aren’t here to be happy. Happiness has the half-life of the time to finish your ice cream. We are here to experience fulfillment. That fulfillment has a cost - sometimes it is requires a sacrifice. However, if that sacrifice is aligned with your money mindset, then it should be accepted and gratifying.

In summary, Money and Trust are a currency to buy fulfillment in balance how we reduce pain, enjoy life, and attend to our responsibilities. However, none of this will come to fruition without a language that is more aligned with your conversation. Say yes to $ and priorities or continue on a rudderless river with % and goals.

Great article, JC! Might borrow some of this (with attribution) in a future article of my own...